MoneyMatch is no stranger to the fintech industry; in 2015 when Naysan Munusamy and Adrian Yap joined hands to delve into fintech. Then came Fazil Fuad, former Assistant Vice President of Rocket Internet Singapore, and they formed the core team of MoneyMatch.

MoneyMatch is approved by Bank Negara Malaysia under the FinTech Regulatory Sandbox in June 2017 and was the first locally to launch a fully electronic know-your-customer (eKYC) customer onboarding process through their mobile app. In the beginning, MoneyMatch operated as a peer-to-peer currency exchange platform, whereby the platform allows users to transfer and exchange foreign currencies online with other individuals without needing any middle man.

Moving Away From P2P

However, they have pivoted their business model and shifted away from P2P since then—now they just provide a fully digital way to send funds abroad. When questioned why they have pivoted from the P2P model, CEO Adrian Yap mentioned, “We still have plans to operate the P2P model but as we mature and have more experience in the industry, we realised that there is a lot of work and coordination to be done in order to operationalise our P2P vision.” Rather than depending on other individuals to transfer and exchange currencies, the platform now operates with a more direct model, utilising payout partners and banking partners to help fulfill transactions. Furthermore, the MoneyMatch team has begun to also take a look into blockchain technology to make transactions more transparent and efficient.

As the team practices an experimental culture at MoneyMatch and are always trying and testing new things out on a daily basis, one of the things that they experimented early on was blockchain technology, particularly on Ripple blockchain.

Just last year, the startup announced that they have successfully conducted their first ever live cross-border transaction out of Malaysia on Ripple’s blockchain. They were able to successfully process the transaction within several hours via the blockchain network compared to the traditional SWIFT network used by banks which normally takes a minimum of two days or sometimes even longer. “After looking through the various options and permutations, we found that Ripple offered something that we could potentially use to increase our value proposition to our customers,” explained Adrian.

Hence they decided to adopt and incorporate the technology to enable people to send money overseas at a much cheaper and faster rate.

Growing Rapidly Since their official launch in 2017, the platform transacted RM100,000 in June 2017 and has now just passed a total of RM350 million in transactions in December 2018. On any given day, they transact over RM1 million in transfers. “I would say we are growing at quite a rapid pace and we are trying to cross the RM1 billion mark as soon as possible,” Adrian added.

The platform monetises by charging a small free for transactions and a small spread on the exchange rate. Currently, based on the website, for personal accounts, any native currency transfer (sending RM to Malaysia; sending SGD to Singapore) costs RM8 per transaction while non-native currency transfers (sending USD to Malaysia; sending USD to Singapore) costs RM88 per transaction.

Adrian mentioned that they allow market forces to determine the pricing but are always looking at ways to reduce the fees up to the point of it costing nothing in the future.

Their user base has also grown since our last coverage of MoneyMatch in September 2017 when they only had 50–60 individual users and 30 corporate customers, now they’ve grown to about 8,000 individual users and about 300 business users.

“We are focused on perfecting what we are doing at this current moment and giving our customers the best possible experience when moving money for personal or business use,” said Adrian. Rethinking Finance MoneyMatch came in third place in the ASEAN SME Category at the Singapore Fintech Festival 2018, bagging a cool SGD50,000 from the Monetary Authority of Singapore as prize money. MoneyMatch was the only Malaysian representative in the 40 shortlisted finalists and the other two winners in the category included fintech startups from Indonesia and Thailand. Furthermore they were also recognised as Fintech Startup of the Year Award 2018 by Fintech News Asia and Startup Disruptor of the Year Award 2018 by Wild Digital 2018. All of these achievements and milestones didn’t come easy as there were plenty of challenges along the few years since MoneyMatch started.

“I would however, place customer trust as one of the biggest challenges to date that we have faced,” explained Adrian. “It’s not easy to get people to part with thousands, tens of thousands or even hundreds of thousands of ringgit and expect it to show up in another country’s bank account in a couple of hours or days.”

He is however, forever grateful and wants to thank his existing customers for putting their trust and faith in choosing MoneyMatch time and time again over existing banks. “Our motto or ethos has always been ‘Rethinking Finance’ and therefore the ultimate goal of MoneyMatch would be to do finance differently, starting with cross border transfers,” he said. In the near future for MoneyMatch, Adrian won’t rule out launching new services or even being a full-fledged digital bank.

2 Comments

The wrong way to understand cryptocurrencies and the blockchain

As the circle of general public awareness around cryptocurrencies grows further, additional new opinions from newcomers start to get formed around what they represent and what they don’t.

To use an old analogy, cryptocurrencies and the blockchain are like a big elephant. If you come to it with your eyes blinded and not knowing what to expect, your first impression will depend on what part of the elephant you have first touched.

First impressions matter. And one of these first impressions we often hear about cryptocurrencies is bewilderment that they aren’t backed by anything, followed by the deduction: “How do they amount to being worth anything”? Newcomers are deducting these early impressions, based on their partial experiences, as the whole truth. But the reality is far from it.

Then, these distorted thoughts are amplified when we hear a public figure calling “crypto a crock” at a U.S. House hearing, or when we read ludicrous reports trying to explain why “Bitcoin Could Fall Below $1,000,” with preposterous claims like “there is no value in it.”

Matter of perspective Of course, like anything in life, our current traditions influence and limit the optics of how we see things. We are used to governments being the sole sovereign backers of national currency, and we are used to relying on financial institutions as the sole providers of sacrosanctity on financial transactions—because all roads lead to a bank or a government.

However, there is a news flash that changes all of this, and challenges these two long-held traditions. And the stakes are very high on the outcome of these changes.

If you put aside what you don’t understand about the blockchain, you just need to remember the simplest and most fundamental novelty behind it: the valid transmission of transactions without the involvement of financial middle parties. And that is the more important revelation about the new world of cryptocurrency. So, the next time someone tells you: “Cryptocurrencies are not backed by anything, they are like thin air,” your response should be to change the conversation to what the blockchain enables, instead of what cryptocurrencies appear to be. You could say: “For the first time, we have a new technology that allows the final settlement of financial transactions between any two parties without the involvement of financial intermediaries.” Imagine the implications of that statement.

Imagine if financial and value-based transactions for any type of asset could be settled directly from one entity to another, while at the same time maintaining valid records of such transactions.

Doesn’t that give us promise for a new financial system that is more efficient than the current one? This technology is systemically disruptive, which is why it is facing headwinds from incumbents who want to cling to the old system. Attacking status quo won’t work But don’t go down the rabbit hole of critiquing sovereign governments who are the current money authorities, or attacking the banks who currently maintain our accounts and move our money.

Frontal attacks are not useful, and rarely effective.

It is better to surround the incumbents and make their market shares smaller while making them gradually irrelevant, by growing the number of cryptocurrency users and raising the general public’s awareness and openness about the technology’s promise. By opening people’s minds further, the rest will follow.

A new short training course on fintech has been launched to help junior executives in the banking and financial services industry better understand how key technology trends will impact the way they work.

The pilot run of the FinTech Foundation Programme started yesterday with about 20 students. The next run will be next month.

The course, which is held over three evenings and one full day, has been developed by the National Trades Union Congress (NTUC), Banking and Financial Services Union, Singapore FinTech Association (SFA) and Ngee Ann Polytechnic.

The programme organisers said they aim to hold the course at least once a month for up to 30 people each time.

National Trades Union Congress assistant secretary-general Patrick Tay said with widespread digital transformation in banking and finance, professionals, managers and executives in the industry must ensure they have the necessary knowledge and skills to stay relevant and competitive. "We have received ground feedback that there is growing interest in fintech, but workers are overwhelmed by how technical current courses are and the costs involved in undergoing such programmes," he said.

The course fees for the new programme range from $71 to $321 after various subsidies for Singaporeans and permanent residents. For example, Singaporeans aged below 40 who are sponsored by small and medium-sized enterprises pay $121. The full fee is $1,070.

Participants can also use SkillsFuture Credit to pay for the course. SFA president Chia Hock Lai said Singapore is one of the world's leading fintech hubs and there will be new opportunities and job roles arising from technology. "The FinTech Foundation Programme will not only introduce workers to the world of fintech but also plug them into the ecosystem. This is especially useful for workers who are keen to pursue a career in fintech."

Participants who have completed the programme can move on to a FinTech Fundamentals Programme by Singapore Polytechnic and a FinTech Deep Dive series on topics like blockchain, big data and artificial intelligence.

One of those who attended the first day of class is Mr Phua Tien Tim, 65, a junior officer working in branch operations at United Overseas Bank. He said he learnt how fintech is rapidly changing and challenging traditional roles in banking.

In his four decades in the industry, he has seen manual systems progress to full online banking. "Fintech is just another change and step that I will learn to conquer," he said.

SFA and NTUC's Employment and Employability Institute also organised a career fair last night for jobs in the fintech industry. About 100 jobseekers attended the event at M Hotel Singapore.

Creating the next fintech unicorn may be harder than you think. In fact, only 1 out of 10 startups succeed. So what’s the secret of success? Join this VB Live event for first-hand insight into how founders and VCs launch their big ideas and see tangible results, with topics ranging from building a team to sourcing funding, finding mentors, and more.

Innovative fintech companies are continuing to disrupt traditional banking and payments industries. But what are the keys to creating a successful fintech startup and how can they snag a piece of the enticingly lucrative pie?

As more and more consumers move from traditional banking services to new and innovative fintech solutions, huge opportunities are opening up to provide consumers with more personalized and predictive fintech solutions that deliver more engaging user experiences and help consumers better manage their financial lives. With new and exciting solutions in categories such as alternative lending, cryptocurrency and distributed ledger technology, social payments, predictive financial wellness, and wealth management solutions, there are a slew of new and disruptive solutions emerging every day.

Today’s consumers are digitally savvy and are increasingly embracing fintech globally with adoption more than doubling from 16 percent in 2015 to 33 percent in 2017. And, over half the banking executives at traditional financial institutions are feeling the threat, and it’s significant.

The time is right for fintech startups that can change the game, but before you throw your hat in the ring, there are some key strategies you need to keep in mind, a vision to clearly outline, and some hard truths to take into consideration when breaking into the category.

The advantage that fintech companies have is that when you offer the kind of deeply personalized user experiences that consumers are looking for, you have a wealth of data and analytics at your fingertips to strengthen your offering and drive more successful marketing and engagement strategies for both current and new customers.

Anticipate fintech trends There are a few key ways to dig in to the fintech field and uncover opportunities, whether they’re new ways to offer old services, or flat-out category disruptors.

Rethink traditional economics

The old-fashioned way of offering financial services can be expensive; digital technologies are transforming systems and processes, and introducing alternative business models, like ad monetization and referral commissions, making it possible to offer these products or services for free. Technology can also lower costs across the board for fintech companies, whether that’s cheaper and more efficient customer acquisition and engagement, a reduction in operating costs, or the ability to offer attractive, sophisticated applications at unexpectedly low rates.

Find the unmet needs

Artificial intelligence and machine learning have unlocked new ways for fintech companies to help their customers’ improve their financial lives. Predictive analytics can help customers find new ways to invest, save, manage spending, and more. And today’s customers are hungry for these personalized and predictive applications, and are actively looking for new solutions to help manage their money and create better financial outcomes. Collaborate Financial institutions still offer a lot of advantages for consumers, plus there’s consumer inertia to overcome — why move your money when it’s doing just fine where it is? So collaborating with the old guard can open up new market opportunities. Fintech companies can bring in new technologies that offer these traditional institutions competitive advantages in a field where consumers are demanding more digitally savvy solutions.

Whether it’s a partnership or a joint venture, this kind of relationship is a frequent launchpad for successful fintech startups.

Lyft prices IPO shares at $72 and will make its Wall Street debut with a $21 billion valuation3/29/2019

Lyft priced its IPO at $72 per share Thursday evening as the ride-hailing company prepares to start trading its shares publicly on the Nasdaq early Friday, the company announced.

This puts the company’s price at the high end of its previous range of $70 to $72 price range disclosed by the company on Wednesday in an amended S-1 after nearly two weeks of road-show conversations with investors made clear that Wall Street’s appetite for shares is high.

At $72 per share, the company will raise roughly $2.69 billion in capital, and make its Wall Street debut with a valuation of nearly $21 billion.

The company will list early Friday on the Nasdaq under the ticker symbol “LYFT”.

At $72 per share, Lyft’s IPO price is a full $10 above the low end of the $62 to $68 range the company first disclosed at the start of its roadshow on March 18. Investor demand was high, and the IPO was reportedly oversubscribed early into its two-week long pitch to potential investors.

In addition to raising it’s price, Lyft raised the number of shares in the offering between Wednesday and its official pricing announcement on Thursday.

The IPO is being closely watched as a test of Wall Street’s appetite for a new crop of fast-growing, but money-losing sharing-economy businesses. Uber, the world’s largest ride-hailing company, is expected to list shares in an IPO in the weeks after Lyft’s offering.

Warren Buffett is still a big Apple bull, but he famously uses a flip phone instead of an iPhone3/29/2019

Apple shares fell by as much as 2.2% on March 25 following its star-studded event, during which it unveiled new subscription services for TV, gaming, and news. But that doesn’t concern renowned investor and Berkshire Hathaway CEO Warren Buffett.

When speaking with Yahoo Finance editor-in-chief Andy Serwer on Monday, Buffett said that “if you have to closely follow a company, you shouldn’t own it.”

That’s because Buffett sees Apple as a long-term investment. “If you owned the best auto dealership in town, the best brand, you wouldn’t drop by everyday and say you know, ‘How many people have come in today?”‘ he said to Yahoo Finance. “You buy it knowing there’s 365 days a year, and you’re going to own it for 20 years, so that’s 7,300 days, and things are going to be different from day to day and year to year.”

Buffett’s Berkshire Hathaway owns a 5.4% stake in Apple, but he famously doesn’t use the company’s biggest product -the iPhone. Buffett uses a Samsung flip phone, which he showcased on CNBC’s Squawk Box last year. It’s unclear exactly what type of phone Buffett uses, but CNBC’s Fred Imbert pointed out on Twitter that it looks a lot like the Samsung Haven. “Tim Cook sent me a Christmas card again this year saying he’s going to sell me an iPhone this year,” Buffett said to CNBC. “He keeps sending me these reminders every Christmas.”

Buffett himself is evidence that the smartphone market isn’t saturated just yet. “When I actually buy it, it’s all over, folks,” he said to CNBC in reference to the iPhone. “The last person has bought it.”

Apple took the wraps off its long-rumored TV service on Monday, Apple TV Plus, which provides access to a slate of high-budget Apple original productions. The company is working with talent including Oprah Winfrey, Reese Witherspoon, Jennifer Aniston, Steve Carell, Steven Spielberg, and Jason Momoa among others, all of which appeared at the event to discuss their upcoming projects that will be part of the service. Apple also debuted a redesigned version of the Apple TV app, an Apple Arcade gaming service, and a paid tier of Apple News that grants access to content from magazines, newspapers, and digital outlets.

But the event left Wall Street with several unanswered questions, particularly around the pricing for Apple TV Plus and Apple Arcade. The event was being closely watched as a major effort by Apple to bolster revenue from its services business as it grapples with slowing iPhone sales.

“As far as this event is concerned, I think there was an expectation that we would get answers to a number of things we didn’t get answers to,” Angelo Zino, an equity analyst at CFRA, told Business Insider sister site Markets Insider. Even if Apple’s TV service doesn’t turn out to be a blockbuster hit, the company can afford to “make a mistake or two,” Buffett recently told CNBC. “I’d love to see them succeed, but that’s a company that can afford to make a mistake or two,” he said. “You don’t want to buy stock in the company that has to do everything right.”

KUALA LUMPUR, MALAYSIA – Media OutReach – 18 March 2019 – Global professional recruitment consultancy released its Michael Page Malaysia Salary Benchmark 2019 citing keen interest from companies to attract professionals within Big Data, data science, consumer insights and data warehousing.

May Wah Chan, Director at Michael Page Malaysia comments, “Malaysia’s digital economy is on the fast track for 2019 which have led to the spike in demand for these key positions. Across industries, companies looking to ride the wave of digital transformation to ramp up efficiency and productivity is creating more pressure on the country’s already tight candidate pool.”

As a result, talent movement in the technology space is anticipated to be exceedingly swift where professionals will experience concurrent multiple offers. The report indicates a 30% increase in the number of technology jobs posted in Malaysia in the last 12 months. Successful job movers in this space can expect a 10 to 22% salary increase.

Malaysia’s development around ecommerce also posts exciting job prospects in 2019. With heavy investments from market leaders, Grab and Alibaba, this has given rise to the need for cybersecurity experts.

The country is moving rapidly towards a cashless society. WeChat mobile wallet is now live in the country, which marks the service’s first expansion outside of China and Hong Kong. Together with Alipay and Samsung Pay, these players will disrupt Malaysia’s e-payments space.

Malaysia’s rapid Fintech development in tandem with Bank Negara’s vision to evolve Malaysia into a complete digital payment society, has sparked a boost in mobile applications, artificial intelligence and robotics.

May Wah observes, “Financial services institutions are on a clear drive to enhance user experience in order to keep their competitive edge. In order to achieve this, they have turned their investment towards technology and the talent required to effectively implement mobile banking and virtual customer service platforms. Staying ahead with technological advancements is also the key to attracting professionals who regard this exposure as important career development.”

Why independent boards are a clear benefit of investment companies.

Individual investors may feel overcharged and undervalued by some financial organisations that seem to be more interested in the weight of money wielded by institutional investors. But shareholders in investment companies enjoy valuable protection built into the structure that is currently unavailable to investors in any other form of pooled fund.

Who looks after individual investors? Independent directors of investment trusts, that’s who.

What do these directors do? Unlike unit trusts and open-ended investment companies (OEICs), investment trusts operate under company law and are led by a board of directors who have a legal obligation to represent the interests of all shareholders, who are the owners of these companies. How do boards of directors deliver value to shareholders? First, by exerting downward pressure on fund managers’ fees, thus minimising costs borne by shareholders. Second, where necessary, by sacking fund managers whose performance disappoints, thus seeking to maximising returns to shareholders.

Fine words, but where’s the proof they are put into action? More than a third of investment trusts have cut management fees in the last five years. Replacement of fund managers – who are hired and fired by boards of directors – is a rarer event but remains a beneficial ‘stick’ to balance the ‘carrot’ of bonuses.

Leading analyst Simon Elliott of the stockbroker Winterflood recalled a few recent examples. He told me: “We believe that the board of what was Schroder UK Growth and is now Baillie Gifford UK Growth made a decisive move in appointing Baillie Gifford as its investment manager, which is reflected in the fund’s subsequent re-rating. “Another positive development, in our opinion, is the pending merger between Standard Life UK Smaller Companies and Dunedin Smaller Companies. Both boards involved have been supportive of this move and we believe it makes sense to consolidate the vehicles, which should lead to better market liquidity while its ongoing charges ratio should fall.

“The case of John Laing Infrastructure’s acquisition is an interesting one, as is the role of its board in accepting the offer. We can see the board’s argument that the offer represented a premium that was equivalent to several years of expected returns.”

Another shrewd observer of the stock market, Alan Brierley of wealth managers Canaccord Genuity, pointed out: “Schroder Asian Total Return and Monks investment trusts both had their fortunes reinvigorated as a result of decisive action taken by their boards after many years in the wilderness. “Schroder Asian Total Return’s board addressed a poor performance record by introducing an outstanding management team with an innovative approach to portfolio construction. The team has since continued to deliver truly exceptional long-term risk-adjusted returns. “The market capitalisation has risen by more than 50% since the beginning of last year and this has improved marketability and lowered the ongoing charge. We also welcome the recent reduction in management fees.

“At Monks Investment Trust, the past three years have seen a dramatic transformation of fortunes. In March 2015, the Board appointed Baillie Gifford’s Global Alpha team and there has been a significant reversal in supply/demand dynamics which has seen a 12% discount to net asset value move to a 1% premium.”

Much of the work of directors is less dramatic but also important, as James de Sausmarez, head of investment trusts at the asset manager Janus Henderson explained: “The board challenges and questions, they ask why a fund manager is doing what he or she is doing – and I think managers enjoy the interaction. “If you are an individual investor, it’s enormously comforting to know there is a group of diversely skilled people overseeing the manager. Mutual funds – such as unit trusts and OEICs – don’t have the same level of challenge.”

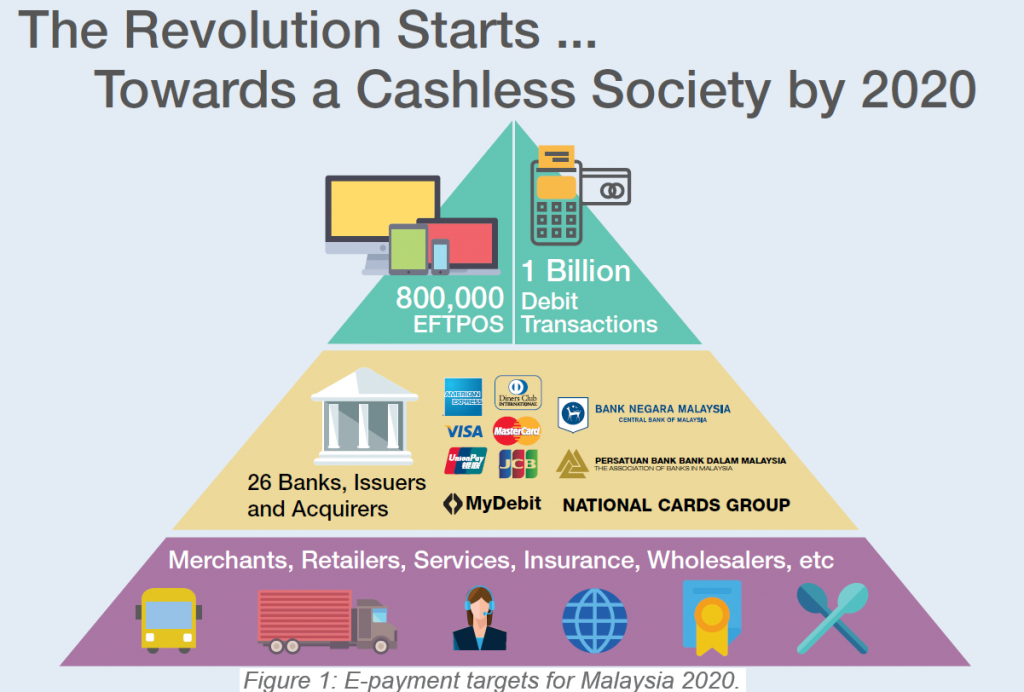

Between Bank Negara Malaysia’s (BNM) ICTF and the more recently announced Real-Time Retail Payments (RPP) system, an ecosystem rife with Malaysians with at least a debit card, and e-wallets to target those who do not; Malaysia seems to be well underway towards becoming a cashless society.

BNM even has a 10-year plan that will culminate in 2020 with the following as a goal:

This is all part of BNM’s goal towards accelerating the country’s migration towards e-payments, and in turn, allow the nation to save paper costs and increase efficiency of the nation’s payment systems.

The bank is working towards increasing the number of e-payment transactions, with each person in Malaysia, on average, making 200 transactions per person, as opposed to the initial 44 transactions per person when the initiative began.

BNM also aims to cut down cheque use by more than half from 207 million, to 100 million per year. Measures to achieve this aim include providing the right price signals to encourage the switch from paper-based payments to e-payments, and facilitating wider outreach of e-payments infrastructure, such as point-of-sale terminals and mobile phone banking.

Where Malaysia’s Cashlessness Stands in 2018

As for transaction volumes per capita, 2018 saw e-money being used most often, at 58.4 (56.2%) times per person on average. The next most frequently used method of payment is via internet banking, at 18.7 (18%) times per person on average. However, the values of these transactions paints an interesting picture. At 333.4 (0.23%), the total value of e-money use does not stand a chance against internet banking’s 140,426.8 (95%), or even credit cards 4,110.2 (2.8%). This shows that as far as user behaviours go, Malaysians use e-money to pay for small transactions rather frequently. While much of the high-value payments in 2018 are done via internet banking. The values for internet banking may be emboldened somewhat by the fact that many Malaysians make payments for their cars, home or insurance via internet banking.

The value for credit cards would probably be higher if more Malaysians owned credit cards. Credit card ownership as of 2018 totals at approximately 10.3 million as opposed to 42.5 million debit card users.

Cash in Circulation is Still HighBetween 2014 to 2018, the amounts of cash in circulation continues to rise despite efforts towards cashlessness. However, the chart above shows an obvious decline in the amounts of cash added into circulation between 2017 (92, 347.6) to 2018 (94,307.2). There are the beginning pinpricks of digital payments’ effect on cash, but we are far from a cashless society as of now.

Here’s How Malaysia did throughout 2018

Credit card transactions throughout 2018 remains relatively stagnant, with an expected increase near the end of the year thanks to Christmas and end-of-year breaks that spurs Malaysians to go out more often. Debit-based transactions however, saw a notable spike throughout the year that more definitively hints towards BNM’s advocacy bearing fruit. Compared to credit cards, it’s easier for Malaysians to acquire debit cards. Furthermore, BNM’s advocacy efforts may have spurred more retailers to bring card readers into their retail businesses. 2018 also saw a higher number of SME merchants like smaller mall kiosks adopt the AirPOS by GHL card reader, which makes it easier for them to accept payments.

Meanwhile, the volume of transactions for e-money somewhat shows an upwards incline, but the volumes remain erratic perhaps based on what e-money issuer has just gained critical traction, or periods of more cashbacks and promotions. As of now, many Malaysians still only opt for e-wallets or e-money when there are discounts or cashbacks that make the product more enticing.

The value, as described above remains small compared to volume of e-money transactions, and does not seem to tally with the volumes either. Clearer indications may appear in 2019, as the e-money scene continues to mature in Malaysia. We wouldn’t count Malaysia a cashless society just yet. Though we may overshoot the 2020 goals as outlined by BNM, Malaysia does seem to be well on its way towards cashlessness. Before the trend hits critical mass, Fintech News has outlined some concerns we should contend with so that Malaysia can reap the cashless benefits without inviting too many of the problems that may arise.

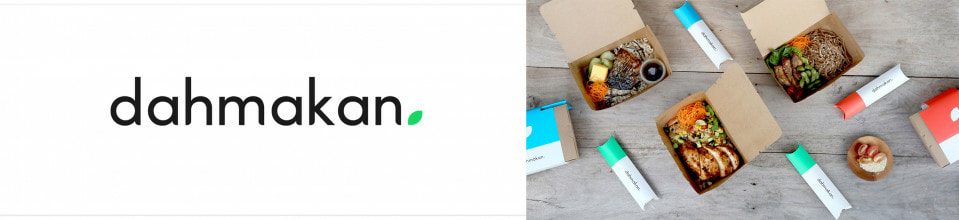

Dahmakan, a Kuala Lumpur-based food delivery startup, acquires Polpa to expand into Thailand3/27/2019

Dahmakan, a vertically-integrated Malaysian meal delivery startup, announced today that it has acquired Polpa to enter Bangkok. Dahmakan was the first Malaysian startup to participate in Y Combinator and recently received a $2.6 million round of funding earmarked for its expansion into new markets.

The company, which was launched in 2015 by former Rocket Internet executives, says it now delivers tens of thousands of meals each month in Kuala Lumpur, where it is based, and Bangkok. Co-founder and chief executive officer Jonathan Weins told TechCrunch that Dahmakan plans to venture into other Southeast Asian markets first, including Jakarta, Singapore, Hong Kong and Manila, before tackling East Asian countries like Japan and Korea.

Polpa was founded in 2014 by Julian Timings and Prongfa Uennatornaranggoon, who will join Dahmakan’s team. Polpa will continue to operate under its own brand in Bangkok.

“Polpa has incredible founders and we have been in touch with them for over a year. We shared the same excitement and wanted to do something much bigger together, so when it came to an acquisition, it made sense because they are complementary to us,” says Weins.

Polpa shares a similar business model to Dahmakan that helps them differentiate from “traditional” food delivery startups like Foodpanda (which was formerly owned by Rocket Internet) and Uber Eats. Self-described “full-stack food delivery” companies, they handle almost all parts of their business operation, including food preparation and logistics, in-house.

In order to make that possible, Dahmakan pre-plans menus a week in advance, offering a choice of several meals each day that customers can order a la carte or with discounted package deals. To make large-scale meal production and delivery efficient and affordable, the startup relies on its proprietary machine-learning routing technology. The system allows it to produce and began delivery of more than 1,200 fresh meals in an hour, or a “four times higher efficiency than the industry benchmark set by Chipotle,” Dahmakan claims. The company also says its delivery cost is five times lower than traditional food delivery companies.

As it expands, Dahmakan will need to compete with other vertically-integrated food delivery services, the most notable of which is probably Grain in Singapore. Weins says Dahmakan’s AI-based technology will be its key differentiator, because it keeps costs down while ensuring quick deliveries.

Dahmakan will also be up against Foodpanda, Uber Eats and other services that offer food from a wide range of restaurants, but Weins says the benefit of choosing from Dahmakan’s pre-planned menus is quality control. Many of its chefs formerly worked in luxury hotels, including Shangri-La Kuala Lumpur, and create meals that the company says would be 30% to 50% more expensive when ordered from restaurants that aren’t able to utilize its economies of scale. |

CORWIN GROUPLatest News Archives

October 2021

CategoriesBy submitting this form, you provide consent for Corwin Group to email you occasionally with industry news and promotions. You may unsubscribe from these emails at any time.Testimonials & Disclaimer

Important Disclosure: By visiting this site, you agree to be bound by CorwinGroup’s Terms of Use and Privacy Policy. CorwinGroup.com is intended for accredited investors and otherwise qualified investors who understand and accept the risk associated with private investments. Investing in private investments on CorwinGroup involves risks, including, but not limited to market and industry risks, risks related to a specific property, currency fluctuation risk and liquidity constraints. Investments are not bank deposits and are not guaranteed. There is a potential for loss of part or ALL of the investment capital. CorwinGroup does not endorse any of the opportunities that appear on the site, nor does it make any recommendations regarding the appropriateness of particular opportunities for any investor. No correspondence or information provided on CorwinGroup.com or by any representative of CorwinGroup should be construed as a recommendation of a security. Each investor is advised to conduct his/her own due diligence as CorwinGroup does not provide any investment advice, business advice, or tax or legal advice. CorwinGroup is not registered under the Securities & Futures Act or the Financial Advisor’s Act. Neither the Securities and Exchange Commission in the country nor any federal or state securities commission or any other regulatory authority has recommended or approved of the investment or the accuracy or inaccuracy of any of the information or materials provided by or through the website. Please read Corwin’s Terms of Use for more detailed terms and conditions to which users of CorwinGroup are subject.

|

RSS Feed

RSS Feed