|

When I emailed you about the ClickFunnels certification class before I forgot to mention one thing… It takes work to get high-paying clients. You have to actually be able to deliver results. If you spend any time on Facebook, then no doubt you’ve noticed recently that more and more marketing consultants and experts are advertising their services. And I believe that 90% of them are dangerously unqualified to be giving out marketing advice.  See most people will go get results in one field, with one winning funnel, and suddenly they’ll assume they’re qualified to give advice to EVERYONE in EVERY niche! Which is ridiculous of course. And so then they get a bunch of clients who buy into their program, and none of their clients get results… but it takes 4 or 5 months before the clients realize they won’t be making any money from what that “expert” told them to do… or set up for them. The reason so many people are able to get away with doing this is because the online marketing world is sort of in a “gold rush” period right now. It’s easier than ever to hyper-target specific sub groups of people with Facebook ads, and thanks to tools like ClickFunnels it’s also super-easy to create an automated sales process. Now, imagine you could get in on that gold rush… Without leaving a bunch of pissed off, betrayed and frustrated clients in your wake… In other words, imagine if you could actually get people results. Then, you’d be EXTREMELY valuable, right? Word would spread quickly about the amazing experience of working with YOU… … and you would quickly start to turn clients away because you were too busy… What would that feel like? Seriously, close your eyes and picture it now… just feel that success flowing in your bloodstream like an addictive drug right now… Feels nice, right? Well, if you’re willing to do a bit of work and learn the proper way to go about this, then you can get all that. Just go register for this training and make sure you attend, then you’ll see just how easy it can be for you to become a highly paid online marketing expert. Go register now, and let me know what you think after you watch it.

Thanks, Corwin Lim

0 Comments

So, the book has been live LESS then 12 hours, and they are FLYING off the shelves. We only had 10,000 at our shipping warehouse, so we just put in a second order (which will take up to 4 weeks to get), but if you want one of the first 10k copies... then NOW is the time.  "Expert Secrets: The Underground Playbook for Creating a Mass Movement of People Who Will Pay for Your Advice..." And I got you a FREE copy (you've just got to cover shipping). Thanks, Corwin Lim P.S. In case you're on of those people (like me) who just skip to the end of the letter, here's the deal: Russell is mailing you a physical copy of his new book. The book is free, and all you pay is the shipping costs. There's no catch... no gimmicks... You will NOT be signing up for any "trial" to some monthly program or anything like that.

The financial services company is expanding its consumer engagement efforts through the deployment of AI-informed bots.Mastercard announced today at the Facebook Developer Conference the release of its newest customer service strategy — a Masterpass-enabled bot via Facebook Messenger. The chatbot will encourage customers at The Cheesecake Factory, Subway and FreshDirect to order through the messenger platform for a frictionless shopping experience.

Using artificial intelligence, the bots facilitate consumers to connect directly with merchants to build and safely checkout via Masterpass without needing to stray from the popular messenger. The strategy is an effort to align with consumers where they heavily spend their time: social media. The bots will support Masterpass-enabled wallets from banks such as Citi and Capital One.

“The Mastercard vision is to support all forms of commerce — addressing the full range of merchant experiences and consumer needs, and ensuring that every one of our accounts is as digital as the people using them. Masterpass-enabled bots on Messenger offer both merchants and consumers innovative, compelling and secure digital payments on an extremely popular and active platform,” said Garry Lyons, chief innovation officer of Mastercard.

This isn’t the first bot deployed by Mastercard. Earlier this year, it opened its Masterpass Chatbot API on its developer platform to support merchants in their experimentation with the technology while also expanding its solutions through multiple channels.

Retailers and brands are turning the corner to embrace new technologies and solutions for enhanced consumer experiences while increasing opportunities to capture real-time data on shopping behaviors. Just today teen retailer Rue21.com announced its virtual stylist bot, also available via Facebook messenger.

“Our bot for Messenger, deployed in more than 26,500 U.S. Subway restaurants, is the largest deployment of a Messenger bot in the restaurant industry. We’re proud to offer our guests an innovative new way to order and pay outside the restaurants,” said Carman Wenkoff, Subway’s chief information and digital officer. “This is a new initiative in the quest to enhance the guest experience.” As consumers begin to shift more of their perusal to mobile devices while also crowd-sourcing product popularity before completing a purchase, providing streamlined bots to bolster secure and seamless checkouts will build brand loyalty from nothing if not convenience and intuitive item discovery.

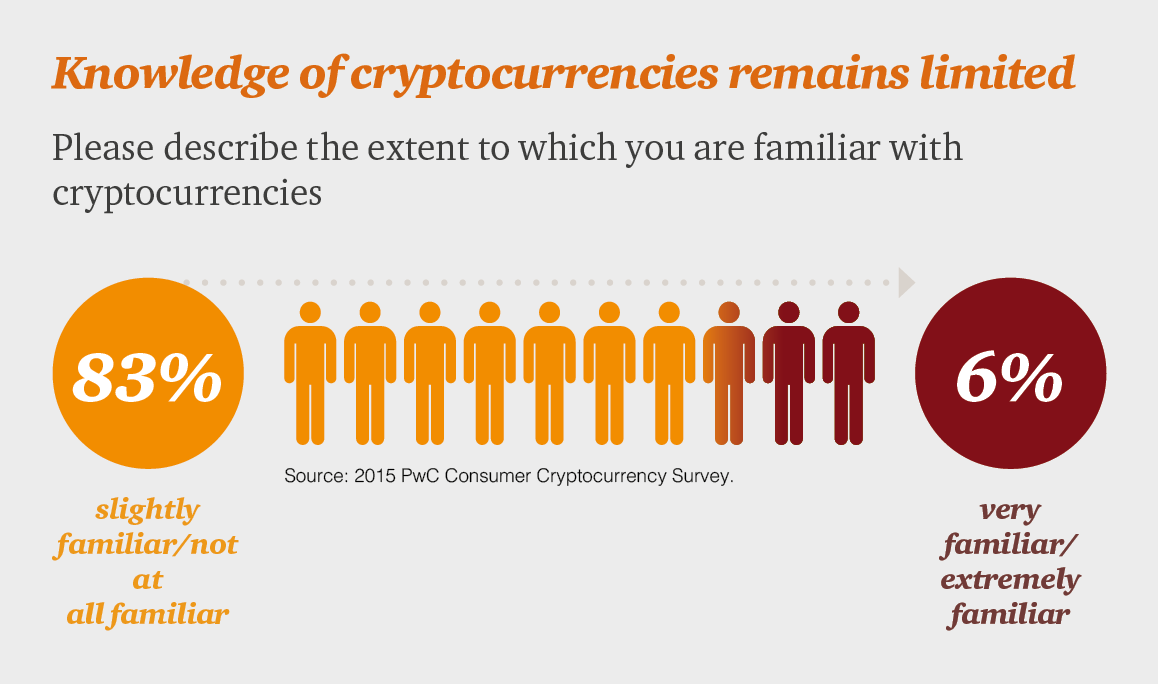

Speculators flocked to Bitcoin and many of the alt-coins in hopes of getting in early and making a big exit, but everyday users haven’t warmed to cryptocurrencies.

There are many reasons why, but one of the largest barriers to mainstream adoption is the price volatility of cryptocurrencies. So the question is, why do the prices change so much in the first place? It comes down to supply and demand: Most cryptocurrencies have only a fixed total supply, and yet demand for the coins is uncertain and constantly fluctuating thanks to speculation. Of course, it’s easy enough to talk about the problem — coming up with a solution is quite another matter.

Why is stability so important?

The need for stability is not unique to cryptocurrency. Any currency needs to be stable in order to be used as a trusted medium of exchange. The more that prices rise and fall, the more ordinary people will shy away from using the coins for everyday transactions. Whether they hoard the coins in the hope that prices will rise sharply soon, or they avoid using them altogether for fear that they will lose all of their value, people are not yet accustomed to seeing cryptocurrency as real money. Worse, the unpredictability of prices wreaks havoc on regular money services, like remittance, currency conversion, and the use of ATMs. In order to use cryptocurrencies, businesses have to hedge their risks by charging exorbitant fees. Bitcoin ATMs can charge up to 15 percent just to convert to fiat currency. This totally defeats the original purpose of cryptocurrencies, which was to offer a cheaper and more flexible alternative to other payment methods. With no advantage over government-printed money, why would the average person use them?

Patience is a virtue

Price volatility has plagued Bitcoin from nearly the beginning. With what we have learned over the better part of a decade, why have cryptocurrencies still not solved this problem of fluctuating prices? Human nature gets in the way, as it tends to do. It is difficult to stabilize prices in a world where people would rather play the market and get instant gratification by re-selling their coins for as high a price as possible. Without careful planning from the very onset of a cryptocurrency’s existence, it’s hard to recover from the effects of speculation.

Phase 1: Building a stable ecosystemWhen building a cryptocurrency from scratch, you first need a solid foundation. From this foundation, the currency can grow and self-correct as it develops.

Gauging demand The first piece of the puzzle is being able to reliably predict demand. Uncertainty around demand is the main cause of price fluctuation, as every user’s intentions are a mystery to every other user. Having a way to gauge real demand for a coin would go a long way in fixing this problem. The issue with predicting demand, though, is the existence of speculators creating artificial demand. This is the core of the problem: With so much speculation, the price for the cryptocurrency will not reflect its actual usage and demand. It simply becomes a bubble that is constantly on the verge of bursting, and no one wants to risk their hard-earned money on that. Traditionally, the solution to the problem of stability was to have a central bank. The government could then alter the money supply at will, for example by causing inflation. Cryptocurrencies are by definition decentralized — that is part of their advantage — and without a central bank they need an entirely new approach when it comes to squashing volatility. They need to do this without compromising the freedom of the users and without resorting to inflation. Cooperation over competition: A decentralized community “United we stand, divided we fall.” What if there was a currency that encouraged people to cooperate? What if people were incentivized by a spirit of growth, rather than of greed? Under the ideal model, a network of cooperative businesses and services would coordinate with each other as a single unit. The coin would be shaped democratically by this co-op (shaped not controlled). Every user would have incentives to help the network grow as a whole, and the use of a blockchain would help make the process be fair. Instead of rampant online speculation, users would visit local exchanges to buy and sell the currency. The community as a whole would vote on when to increase the coin’s price, which would keep things democratic and guard against sharp spikes. Official local exchanges Having to look other users in the eye can make a world of difference. Face-to-face exchanges at trusted locations means that the sale of a coin can be more easily limited, and this can act as a throttle to gauge demand. People on the “front lines,” seeing the real demand for the coin in person, can then vote to increase the price. Having stable locations to exchange the currency also creates consistency. It removes the guessing game of wondering where you can buy and sell your coin. The advantages are not just purely economic, either. Cryptocurrencies don’t exactly have the best reputation thanks to their penchant for attracting unscrupulous people. Unethical or illegal businesses will tend to be voted out of cooperative networks with face-to-face exchanges, however, which can go a long way toward legitimizing the currency. It would still be possible to run such enterprises of course, but they would never be part of the co-op. Local exchange dominance This kind of approach can only work if there are dramatically more local exchanges than online exchanges. It would mean that the local exchanges would dictate the pricing of the currency. Marketing early can be disastrous Marketing is a powerful force, and as such it needs to be handled with care. On the one hand, founders naturally want to attract investment early on. This will raise the price of the coin and help pay for infrastructure, as well as boost the growth of the coin. On the other hand, historically the earliest investors in cryptocurrency have been extremely low quality — they are the speculators who doom the currency in the long run and scare away mainstream users. With speculation, capital infusion is needed to keep the currency stable, which can be a significant task. Take Bitcoin for instance: With a market cap of roughly $20 billion, it would need a huge amount of capital to have a stable floor.

Slow and steady wins the race

Cryptocurrencies are still in their infancy, and it’s hard to tell where the path for most of the major currencies is headed. What is the “finish line” that they are aiming for? What will the end game be? Most cryptocurrencies have little direction besides the whims of the market, so there’s no telling where they will end up. However, there are a handful of interesting coins that have invested in strategies that nudge them in a specific direction. The central app coin method This is a strategy that is centered around creating value with unique products and services that are associated with the currency. In this way, you could say that the currency is backed by something that people actually want. For example, the MaidSafe network incentivizes users to provide something of value to the network (storage space), and offers the use of apps and services in return for coins. This naturally leads to better cooperation. People want to create value and channel their efforts toward the growth of the currency that they have in common. The setup and switch method Similar to the central app strategy, this method establishes a user base first, and then introduces the currency. Bitshares and its array of associated startups is a good example of this. Several networks with varying currencies — Steemit and their STEEM currency, Peerplays and their tokens, for instance — slowly built their user base and value exchange system, and now they plan to adopt a central currency with Bitshares. This allows them to create a stable base first before pooling their resources. The grassroots movement Finally, the best way for a currency to create that all-important foundation of true users is through bootstrapping. Just like a business startup, a currency like this would need a user base that believed in a common mission. It would need everyone in the system to be able to see the inherent value of the coin, and to understand that it could be worth much more than the value it is traded for in its early stages. An example of one of these grassroots efforts is FairCoin. It’s a currency established and led by FairCoop, whose strategy is to build an ecosystem where businesses cooperate to give users maximum value. It is a currency built from the ground up to incentivize the long-term interests of users instead of their short-term greed — not just because it’s the right thing to do, but because it makes sense. FairCoin focused from the beginning on building infrastructure for everyday users. Because of the strong relationships among members of the co-op, they can have thousands of ATMs, debit cards and exchanges that make mass adoption much easier. An approach like this allows the currency to slowly build itself in the background without the need for a spotlight and the barrage of speculators that come with it. This offers the huge advantage of stability from the very beginning, though it does pose the problem that FairCoin has to bootstrap with less capital than most coins. Unlike other cryptocurrencies, they can’t rely on CoinMarketCap to sing their praises by displaying artificially rising prices (the effects of speculation). In other words, FairCoin traded the excitement of volatility and greed for a quiet, long-term stability. The only problem is that people might not notice! Drama catches the human eye, after all.

Hard forks

Let’s take a look at the hard fork that looms in the horizon for Bitcoin. As if things weren’t complicated enough, now there could be two competing chains for the currency. There are already many technical barriers to Bitcoin’s adoption among mainstream users, and this is yet another one. This makes the price even more uncertain, and uncertainty is like poison for a currency. On the other hand, if you have a large community and a co-op on top of an immutable blockchain, then a hard fork is extremely unlikely — and unnecessary. Cryptocurrencies like MaidSafe, Bitshares and FairCoin all represent solid communities that are incentivized to cooperate instead of speculate. This means that the coin can be worth more than its market price; it has a high inherent value within the system itself. This makes it so that users have very little reason to defect from the existing community. A hard fork would mean giving up many benefits of the co-op, so people stay loyal to the original vision of the currency. When something deeper than just greed ties a community, hard forks don’t occur as often. Conclusion Stable prices don’t just happen by accident. They are not a miracle of the market — they require a carefully constructed foundation. A stable currency needs a stable ecosystem first. While it’s tempting to market the currency too soon because capital injection can do a lot to raise prices in those critical early periods, it’s better to wait. Advertising is like opening up Pandora’s box and inviting the world to look inside. Some of those users will be interested in the actual currency, but others will be undesirable speculators that just leech off the system. For a currency to be stable, it needs to be used by “the 99%,” not just a handful of investors. A currency needs to grow with the people, not past them. Look at the state of Bitcoin and its inflated prices. The everyday person can no longer either mine the coin or expect to use the coin in everyday transactions without high fees or risk. It has been given up to the speculators. With a truly stable currency, on the other hand, you can have currency conversion, remittance, ATM withdrawals and other financial services with lower fees than fiat systems. In other words, it can be used as intended — as money. This is what will ultimately attract a mainstream audience and will actually incentivize them to make the switch to cryptocurrency. Written by: Neil Haran, CRUNCH NETWORK Share by: Corwin Group

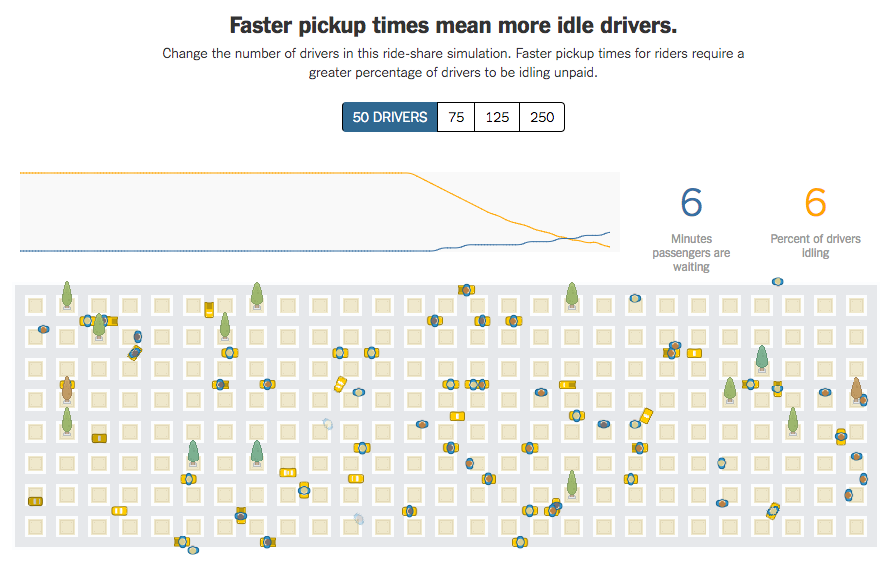

On Monday, the New York Times published an article with a simulation of a rideshare company that included the assertion that “faster pickup times for riders require a greater percentage of drivers to be idling unpaid”:  This is simply not true—and had the Times asked us whether it was, we would have explained the reality of what happens when Uber grows in a city: riders enjoy lower pick-up times and drivers benefit from less downtime between trips. It’s a virtuous cycle that is widely acknowledged in business and academia, and which is backed up by data.  How is this happening? First, as the number of passengers and drivers using Uber grows, any individual driver is more likely to be close to a rider. This means shorter pickup times and more time spent with a paying passenger in the back of the car. In addition, new features like uberPOOL and Back-to-Back trips have meant longer trips, while incentives to drive during the busiest times and in the busiest locations help keep drivers earning for a greater share of their time online. And that should be no surprise: drivers are our customers just as much as riders. So although the Times article suggests that Uber’s interest is misaligned with drivers’, the opposite is true: it’s in our interest to ensure that drivers have a paying passenger as often as possible because they’re more likely to keep using our app to earn money. (And Uber doesn’t earn money until drivers do.) Maximizing the efficiency of cars on the road also helps cities use existing infrastructure more efficiently, while minimizing congestion. Indeed, research from 2016 showed that Uber was already more efficient than pre-existing on-demand options, and we’re excited about those trends getting better over time. So how did the Times graphic get it so wrong? While it’s hard to know for sure as its assumptions are not laid out transparently, it appears to suffer from at least two flaws:

So what does it all mean? Happily, evidence to date has shown that all three things can happen simultaneously: we can grow the overall number of people who have access to work with Uber while reducing wait times for riders and reducing the amount of time drivers spend idling. That’s an exciting set of evidence for the future of on-demand transportation.

Standard Chartered Private Bank has launched a digital wealth advisory tool for its relationship managers (RMs) that integrates the its entire suite of house views and investment recommendations with Thomson Reuters’ real-time market information. ADVICE is powered by Thomson Reuters Eikon, a financial markets information and analytics platform. RMs can now advise clients more quickly and effectively based on an aggregation of the bank’s investment expertise, further supported by Thomson Reuters news and financial analysis.  'This is a significant game changer as it harnesses the full breadth of our advisory capabilities, enabling our RMs to deliver in-depth investment advice to our clients with a much faster turnaround time,' said Alexis Calla, global head, investment strategy and advisory at Standard Chartered. 'Combined with live data from Thomson Reuters, this innovative solution allows our clients to get quicker access to actionable insights through their RMs and respond more nimbly to market events, which is especially crucial in today’s increasingly volatile investment environment.' RMs can access ADVICE via their Thomson Reuters Eikon-enabled desktops, to engage in investment-led conversations with their clients. ADVICE houses the private bank’s actionable conviction lists across equities, bonds, funds, foreign exchange and derivative structured products. It also provides access to the latest news and commentaries across economies, industries, companies and governments. These features will empower RMs to guide clients more effectively in their investment decisions.  Not a day goes by without a media mention about blockchain technology’s potential to change the status quo of how data will be recorded, stored and transferred in the future. As blockchain is booming, investors are taking note and looking at opportunities where they could benefit. Investing in bitcoin, the digital currency built on the blockchain, is considered too risky by many investors and, at the same time, doesn’t actually offer exposure to developments of new blockchain applications and the growth of this technology. Fortunately for investors, however, there are ways to invest in the blockchain boom don’t involve buying bitcoin. Blockchain Startup Stocks Firstly, investors can purchase blockchain startup stocks. Currently, there are several publicly traded stocks in blockchain companies trading on global exchanges. The first blockchain stock that started trading in the U.S. is that of the company BTCS Inc., which provides an online bitcoin shop and a range of blockchain solutions, according to its website. Another prominent North American stock is the Vancouver-based blockchain consultancy service provider BTL Group, which has recently launched its own smart contract platform called interbit. Its stock is trading on the Toronto stock exchange. Outside of North America, there are listed blockchain stocks in the U.K. and in Australia. In the U.K., the London-based blockchain technology investment and development company Coinsilium is listed on the ICAP Securities and Derivatives Exchange (ISDX) and was the world’s first initial public offering by a blockchain startup. On the Australian Stock Exchange, there is the blockchain startup DigitalX. DigitalX provides two blockchain-based services: a global peer-to-peer remittance service called Air Pocket and a software solution to provide bitcoin liquidity to institutional investors called DigitalX Direct.  Crowdfunding Platforms Alternatively, investors can purchase shares in blockchain startups during early-stage funding rounds through online crowdfunding platforms. Young blockchain startups regularly choose the route of online crowdfunding to secure funds to develop their products or service. The crowdfunding platform BnkToTheFuture, for example, allows investors to place funds into a range of Bitcoin and blockchain startups. Notable blockchain startups that have raised funds through BnkToTheFuture’s platform have included the prominent African remittance startup BitPesa and the multi-currency mobile bitcoin wallet Shapeshift.  Invest in New Blockchain Projects’ Initial Coin Offerings The third option for investors would be to invest in initial coin offerings (ICOs) of new blockchain projects. ICOs are a new, innovative way of raising capital that involves blockchain projects issuing their own digital currencies or tokens to early backers during a crowdsale. As this new form of crowdfunding is still entirely unregulated there is substantially more risk involved than investing in blockchain stocks or in traditional crowdfunding campaigns, but the returns of successful ICOs have been excellent. When it comes to investing in ICOs, the key is to select blockchain projects that will have real-life applications and are managed by a team of experienced blockchain developers. Some projects may even have financial backing from leading Bitcoin investors. That is usually also a good sign. Unfortunately, the more the ICO market grows, the more fraudulent activity also occurs. Hence, it is vital to conduct thorough due diligence on each ICO before investing in the crowdsale to avoid falling victim to a scam. As blockchain technology will likely become the standard to securely record, store and transfer data in many industries over the next ten years, it might be wise to start looking into the investment opportunities in this space, despite the potential risk involved in these investments. The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc. At Grab, our dream is to provide everyone with safe, comfortable, and affordable transportation. Today, we’re one step closer to achieving that. Now you can book a GrabCar in Langkawi, Kota Bharu, Kuala Terengganu, and Miri. So you can enjoy rides with Fixed Fares, where the fare you’re given won’t change despite the traffic or route, in even more places. If you’re in these new cities, give us a try today!  Our service is now more accessible than ever before as we are now in 13 cities across Malaysia. Check out all the locations you can book a Grab ride below:   |

CORWIN GROUPLatest News Archives

October 2021

CategoriesBy submitting this form, you provide consent for Corwin Group to email you occasionally with industry news and promotions. You may unsubscribe from these emails at any time.Testimonials & Disclaimer

Important Disclosure: By visiting this site, you agree to be bound by CorwinGroup’s Terms of Use and Privacy Policy. CorwinGroup.com is intended for accredited investors and otherwise qualified investors who understand and accept the risk associated with private investments. Investing in private investments on CorwinGroup involves risks, including, but not limited to market and industry risks, risks related to a specific property, currency fluctuation risk and liquidity constraints. Investments are not bank deposits and are not guaranteed. There is a potential for loss of part or ALL of the investment capital. CorwinGroup does not endorse any of the opportunities that appear on the site, nor does it make any recommendations regarding the appropriateness of particular opportunities for any investor. No correspondence or information provided on CorwinGroup.com or by any representative of CorwinGroup should be construed as a recommendation of a security. Each investor is advised to conduct his/her own due diligence as CorwinGroup does not provide any investment advice, business advice, or tax or legal advice. CorwinGroup is not registered under the Securities & Futures Act or the Financial Advisor’s Act. Neither the Securities and Exchange Commission in the country nor any federal or state securities commission or any other regulatory authority has recommended or approved of the investment or the accuracy or inaccuracy of any of the information or materials provided by or through the website. Please read Corwin’s Terms of Use for more detailed terms and conditions to which users of CorwinGroup are subject.

|

RSS Feed

RSS Feed