|

The beauty industry is changing, and venture capitalists are taking notice.

According to a recent report from Nielsen, 96% of traditional beauty retail channels (meaning brick-and-mortar options) are controlled by the top 20 cosmetics manufacturers—but on the flip side, 86% of ecommerce channels are controlled by companies outside the top 20.

That means smaller ecommerce businesses are dominating the landscape for direct-to-consumer sales and subscription services. And this year more than ever, venture capitalists are looking to get in on the trend.

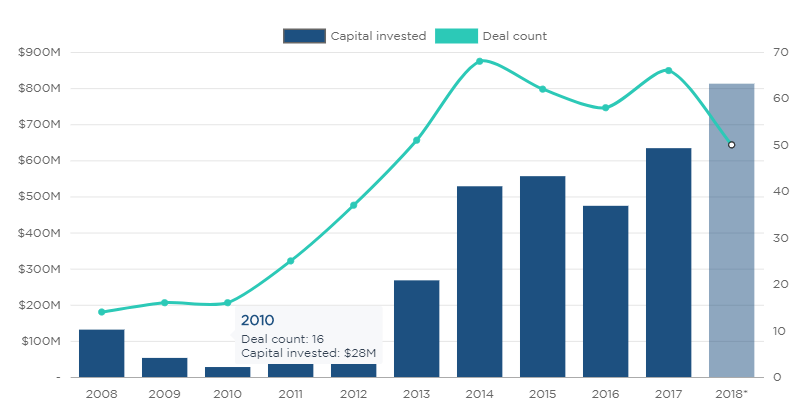

Just over three-quarters of the way through 2018, US-based companies in the beauty industry have already raised a record amount of VC funding, coming in at a total of $812 million and counting, per PitchBook data. Last year's total was about $634 million. Deal count is set to be on par with last year's and almost hit a high reached in 2014. Here's a closer look:

Of the 50 VC deals for beauty companies that have closed so far this year, several have been for companies that sell makeup directly to consumers. Among them are Glossier, which brought in $52 million, and Mented Cosmetics, which raised more than $3 million.

But it's not all about makeup—other types of companies in the personal care sector are also getting in on the funding boom. One of the largest rounds in the space so far in 2018 was a $112 million funding for Harry's, which ships razors and shaving supplies to its customers. Hims, a provider of wellness products including hair loss prevention kits, brought in a pair of funding rounds in the first six months of the year. And fragrance subscription service Scentbird raised $18.6 million in May. So, why are venture capitalists flocking toward beauty companies? It's partly because businesses that specialize in cosmetics and other personal care products are getting good at using technology to sell their products.

Beyond the online platforms brands are building for direct sales, they're taking advantage of social media more than ever. Glossier, for instance, launched its makeup on Instagram before it even had its website. Glossier founder Emily Weiss said at TechCrunch Disrupt last month that more than 70% of millennials purchase beauty and fashion products through Instagram. YouTube is also a major platform for beauty brands. So far this year, an average of more than 1 million beauty videos are viewed on the video site every single day, according to a BBC report. That's up from averages of 800,000 per day last year and about 500,000 in 2016.

Another impetus for investors backing private beauty companies is that they're paying attention to what customers want. Consumers are increasingly drawn toward personalized beauty products, including those that offer a variety of shades for a diverse customer base. Early last year, Shiseido bought MatchCo, a venture-backed startup that makes customization software meant to help users find products that match their skin. Mented Cosmetics specializes in makeup made for darker skin tones. And singer Rihanna is the founder of Fenty Beauty, which provides foundations meant to work with all skin tones.

Consumers are also increasingly interested in buying products from companies that place an emphasis on natural ingredients. NPD Group, a marketing research company, found that the clean beauty market grew by 10% last year, versus 3.8% for the mass beauty industry. Many private companies are catering toward customers who want green, organic products. For example, Goop, which sells personal products through its website, trends toward natural brands meant to enhance wellness. And True Botanicals, which raised about $8 million in VC funding earlier this year, sells natural skincare products.

Whatever a company's focus, the opportunity for ecommerce businesses in the beauty industry is likely to continue to grow. According to statistics portal Statista, ecommerce sales accounted for just about 10% of all global retail sales in 2017, and the share is projected to steadily increase past 17% over the next few years.

0 Comments

As Robert Kiyosaki grew up, he had the unique opportunity of having two father figures in his life who imparted financial advice. One was his actual father — aka “poor dad” — who was educated and worked for others all his life. The other was the father of his best friend — aka “rich dad” — who opted for entrepreneurship instead of formal education.  Kiyosaki’s experience with the two men led him to write several books based on money and investing. Published over two decades ago, Kiyosaki’s book “Rich Dad, Poor Dad” continues to reign as one of the top-selling personal finance books. His unique perspectives on money revealed in the book, as well as his financial success, are the result of being mentored by his rich dad.  The Philippine commercial banking industry aims to capitalize on blockchain to improve money transfer services and promote financial inclusion.  With annual remittances at nearly $30 billion and growing, the commercial banking sector in the Philippines and the country’s central bank, Bangko Sentral ng Pilipinas (BSP), are exploring ways of improving payments and money transfers. One area of interest is the distributed ledger technology (DLT), which is more popularly known as blockchain and underpins cryptocurrencies such as Bitcoin. Speaking at the annual convention of the Philippine Correspondent Bank Officers (APCB), BSP governor Nestor Espenilla Jr. said the central bank was looking for ways to utilize DLT for wire transfers and other traditional banking services.  Espenilla said in his keynote address: “One recent development with significant impact [on] correspondent banking is the rise of blockchain, or distributed ledger technology (DLT). The BSP is working closely with market innovators and industry players to explore tie-ups of correspondent banks with DLT providers. We believe that collaboration and strengthening partnerships with other fintech players is a way to boost digital capabilities of correspondent banks.” Correspondent banks act on behalf of other financial institutions, most often providing services such as facilitating wire transfers, conducting business transactions, accepting deposits, and gathering documents.  “Technology-based solution providers suggest that blockchain or DLT could be harnessed to alleviate some correspondent banking issues. This can be achieved by enabling better risk management, reducing costs, and providing an alternative payment platform, especially in terms of transferring small-value payments,” Espenilla added. The BSP chief made his comments in the wake of a survey showing that nearly 60 million adult Filipinos remain unbanked, which presents a considerable challenge but also opportunities for digital financial inclusion. The BSP 2017 Financial Inclusion Survey (FIS) said that only 15.8 million, or around one-fourth of the total adult population, own a bank account.

On Monday, the BSP reported that personal remittances from Filipinos working abroad reached $2.7 billion in May, or 6.1% higher than the level recorded a year ago. On a cumulative basis, personal remittances for the first five months of 2018 grew by 4.4% year-on-year to reach $13.2 billion.  The Hong Kong Monetary Authority (HKMA), the autonomous Chinese territory's de facto central bank, is poised to launch a live blockchain trade finance platform within two months. "The Trade Finance Platform is a blockchain project initiated by 7 banks in Hong Kong. The project has been facilitated by the HKMA and is targeted for launch by September 2018," the authority told CoinDesk via email.  According to a report from the Financial Times on Monday, the HKMA's blockchain platform has 21 banks participating as participating nodes, including HSBC and Standard Chartered. The project has been public since early in 2017, when reports indicated several banks had completed a test for the trade finance platform, alongside the HKMA, in an effort to bring transparency to data sharing across financial institutions. Participants at the time included the HKMA, Bank of China, Bank of East Asia, Hang Seng Bank, HSBC and Standard Chartered Bank, with consulting firm Deloitte as a facilitator for the project.  "The aims of the platform are to reduce frauds related to trade finance and double financing, and therefore lead to increased credit availability and lowered financing costs in the long run. This may in turn help small and medium-sized enterprises (SMEs) access to trade financing," the HKMA explained today. Aside from the founding banks, other institutions have also indicated interest in the platform, according to the email, and the HKMA expects more banks to gradually join in the future. When and if it goes live, the HKMA project will be one of the first live blockchain trade finance platforms backed by a government institution. Earlier this month, a group of European banks also announced that a trade finance blockchain platform dubbed We.Trade, built with help from technology giant IBM, is also live.  Meanwhile, the HKMA is also working with its counterpart in Singapore to develop a blockchain-based trade finance network to settle cross-border transactions. The two partners previously slateda launch date in early 2019.  The Korea Internet & Security Agency (KISA) and the Korea Housing Finance Corporation (HF) have signed a memorandum of understanding (MOU) to develop a blockchain-based storage system for documents, Korean news agency Newsis reports July 16.  KISA and HF will introduce a blockchain system to manage electronic documents for mortgages and loans. KISA will provide HF with consulting and technology for building and operating the new system. HF, which provides housing finance services for low and middle-income families, will digitize paper documents and migrate them onto an online registered documents storage system. The system also aims to provide blockchain-based self-identification services in order to expand customers’ data protection and streamline the customer experience. HF CEO Jung-hwan Lee said that “We will improve our services so that customers can easily use the products of Housing Finance Corporation on mobile." Founded in 2004, HF is a state-run corporation that, according to its website, promotes the development of the Korean economy by helping provide a stable supply of housing funds. KISAis a sub-organization of the Korean Ministry of Science and ICT which oversees the cybersecurity of the Internet in South Korea.  A range of educational, financial, and governmental organizations have begun to explore blockchain technology’s potential for securely and efficiently storing documents. In late June, a Russian university announced it will store diploma records using blockchain technology to improve document accessibility and authenticity. The Financial University said that all diplomas issued over the last ten years will be recorded using distributed ledger technology. In April, the Russian National Intellectual Property Transactions Coordination Center (IPChain) signed an agreement with the State Patent Office of Kyrgyzstan (KyrgyzPatent) to provide a system for digitizing patent records on a blockchain-based storage system.  In March, major Polish bank PKO Bank Polski announced its partnership with blockchain startup Coinfirm to develop a blockchain-powered storage and verification system for bank documents. PKO bank hopes that the new measure will cut costs, as digitizing client records will eliminate the need for expensive paper documentation for over nine million customers.  |

CORWIN GROUPLatest News Archives

October 2021

CategoriesBy submitting this form, you provide consent for Corwin Group to email you occasionally with industry news and promotions. You may unsubscribe from these emails at any time.Testimonials & Disclaimer

Important Disclosure: By visiting this site, you agree to be bound by CorwinGroup’s Terms of Use and Privacy Policy. CorwinGroup.com is intended for accredited investors and otherwise qualified investors who understand and accept the risk associated with private investments. Investing in private investments on CorwinGroup involves risks, including, but not limited to market and industry risks, risks related to a specific property, currency fluctuation risk and liquidity constraints. Investments are not bank deposits and are not guaranteed. There is a potential for loss of part or ALL of the investment capital. CorwinGroup does not endorse any of the opportunities that appear on the site, nor does it make any recommendations regarding the appropriateness of particular opportunities for any investor. No correspondence or information provided on CorwinGroup.com or by any representative of CorwinGroup should be construed as a recommendation of a security. Each investor is advised to conduct his/her own due diligence as CorwinGroup does not provide any investment advice, business advice, or tax or legal advice. CorwinGroup is not registered under the Securities & Futures Act or the Financial Advisor’s Act. Neither the Securities and Exchange Commission in the country nor any federal or state securities commission or any other regulatory authority has recommended or approved of the investment or the accuracy or inaccuracy of any of the information or materials provided by or through the website. Please read Corwin’s Terms of Use for more detailed terms and conditions to which users of CorwinGroup are subject.

|

RSS Feed

RSS Feed